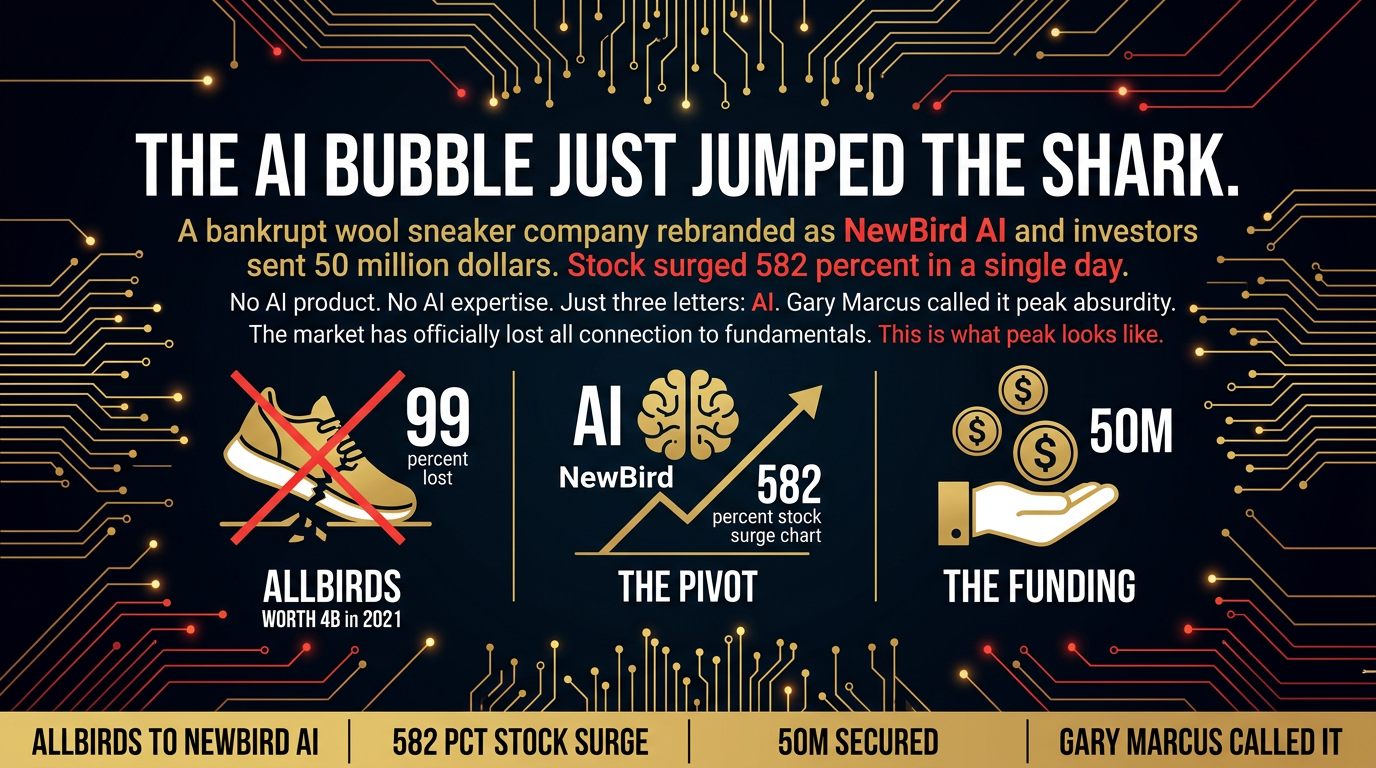

A bankrupt shoe company just rebranded as "NewBird"

A bankrupt shoe company just rebranded as "NewBird AI" and its stock surged 582% in a single day. No product. No expertise. Just three letters. It then secured $50M in funding.

That is not a joke. That is Gary Marcus's latest data point for why he thinks the AI market has hit peak absurdity. Marcus has been calling this wrong for thirty years, by his own admission. He predicted AI would plateau in 2022 and GPT-4 would fizzle. He has been wrong on timelines while being right about problems. The 582% spike in a single day on literally nothing is hard to argue against.

This is not an attack on AI. The underlying technology is real and getting more capable every quarter. This is an attack on the market narrative that has detached from any connection to fundamentals.

The Market Is Pricing Vibrations, Not Value

Allbirds was once worth $4 billion. By 2026 it had lost 99% of that value. The company was facing a $39 million fire-sale. It was done. Then someone in a board room figured out that adding "AI" to the name and pivoting to "acquiring GPUs for AI compute" was worth $50 million from an unnamed investor. The stock surged 582% mid-day trading.

The environmental mission that defined the brand, the public benefit corporation status, the eco-conscious positioning — all of it dropped in favor of a GPU acquisition strategy with no product roadmap, no technical team, and no AI revenue.

Marcus documented the same pattern with Oracle. Stock up 43% on rumors of an OpenAI partnership. Oracle briefly hit $308. Now trading around $170. The partnership was never confirmed. The fundamentals never justified the spike.

When a bankrupt shoe company can raise $50M by adding three letters to its name, you are not watching rational capital allocation. You are watching a market that has confused the technology with the hype cycle.

The Problem With the Narrative

Every dollar flowing into NewBird AI is a dollar not funding a real AI company with real technology and real revenue. The companies actually doing meaningful work are competing against pure speculation. That is a market failure, not a market signal.

Marcus has been documenting this for months. His earlier "Peak Bubble" call on Oracle was met with the same responses you always get when calling a top: too early, wrong about AI, do not understand the technology. Maybe. But watching a bankrupt shoe company raise $50M on vibes is not a sign of a healthy market. It is a sign that capital is chasing narrative instead of fundamentals.

The irony is that infrastructure vendors are actually making money. NVIDIA is printing money. Cloud providers are printing money. Data center operators are printing money. The companies building AI compute infrastructure are capturing real value because AI actually requires compute at scale.

The companies claiming to build on top of that infrastructure are mostly not. The gap between what AI companies promise and what they deliver is measured in billions of dollars of burned capital and valuations that assume利润 by 2030.

What This Means for Small Operators

If you are building a small agency or product business, this market noise has two implications that matter.

First, the companies worth watching are getting drowned out by the noise. Real AI companies with real technology and real revenue are harder to identify when every press release that says "AI" gets a valuation boost. Pay attention to who is actually shipping product and who is riding the narrative.

Second, the infrastructure layer is where the real money is if you are thinking about where to place bets. Not as investment advice. As a business operator. AI requires compute. The vendors selling compute are making money regardless of which AI application wins. If you are building AI workflows for clients, understand who owns the infrastructure, because that is where leverage lives.

The market will correct at some point. Marcus might be early again, the same way he was early on AI plateau. But the Allbirds story is not a sign of a healthy market. It is a sign that capital is chasing narrative instead of fundamentals.

Do not pivot your actual business to chase the narrative. But do understand that narrative is currently driving valuations in ways that will eventually reverse. The companies building real things will still be building real things when the music stops.

Sources: - Gary Marcus — Peak Absurdity Part II - The Guardian — Allbirds Stock AI Pivot - Hacker News Discussion

Comments ()