Mozilla: Open Source AI at 33% Traffic, 4% Revenue

TL;DR

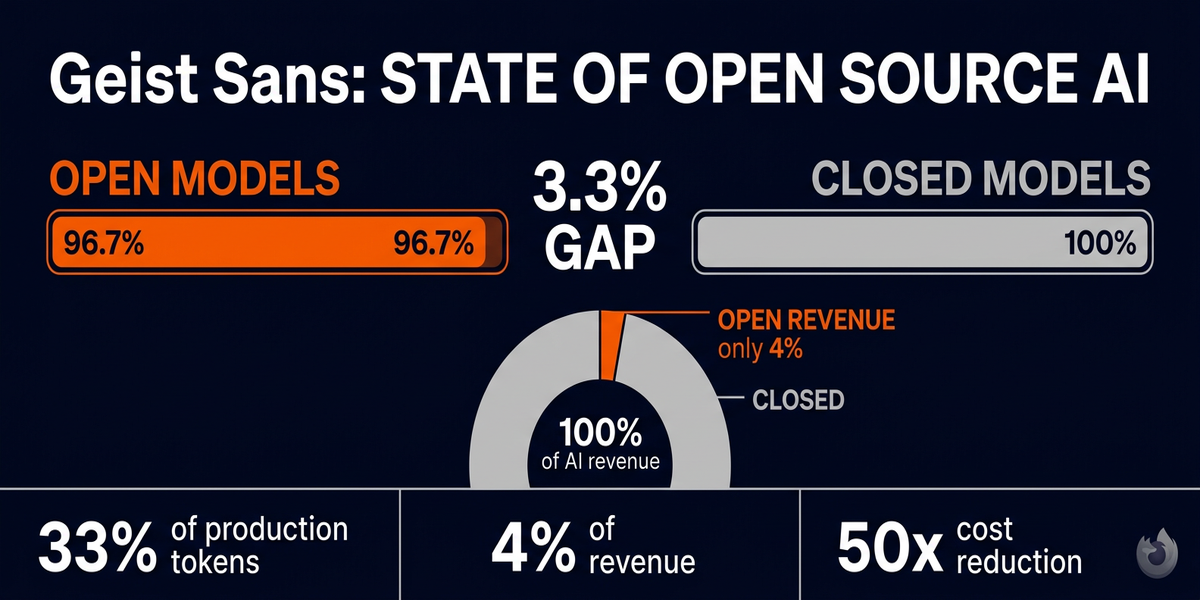

- Mozilla released its inaugural State of Open Source AI report on July 14, 2026, and the findings reframe the open-versus-closed debate. - Open models trail closed systems by just 3.3 percentage points on key benchmarks, down from 8.04% in January 2024. - Open models handle roughly 33% of production tokens but capture only 4% of global AI revenue. Closed providers charge about 6x more per call for comparable quality. - Mistral hit $400 million in ARR (up twentyfold in 12 months). Databricks is running at a $5.4 billion revenue rate. Open-weight models are a real business now. - The real blocker is not model quality. Mozilla points to operational tooling, deployment infrastructure, and trust gaps as what keeps open models from capturing their share of revenue.

Mozilla's first-ever State of Open Source AI report landed July 14, 2026. And the headline finding reframes the open-versus-closed debate for anyone building with AI right now. Open source AI models handle roughly a third of all production traffic worldwide but collect about 4% of the revenue.

Closed providers like OpenAI and Anthropic charge approximately 6 times more per call for comparable output quality on many tasks. And most teams happily pay it.

The performance story is different from the revenue story.

Mozilla's benchmark analysis shows open models trail closed systems by just 3.3 percentage points on Chatbot Arena. The gap was 8.04% in January 2024, narrowed to 0.5% by August 2024, then widened again to 3.3% by March 2026 as reasoning-focused closed models pulled ahead. On coding, instruction-following, and general knowledge, the report puts open models at or near parity. But TIME pushed back on that claim, noting that an acknowledged reasoning deficit means closed models probably still win on complex coding tasks that require multi-step thinking.

Here is what the numbers actually mean for small operators. And why the deployment gap matters more than the benchmark gap.

How Close Are Open Source AI Models to Closed Ones?

The benchmark trajectory tells a clear story over 26 months.

Open models went from 8.04% behind in January 2024 to within 0.5% by August 2024. Then closed models found a new gear with reasoning-focused architectures and pulled back ahead to 3.3% by March 2026. Open models did not stall. Closed models accelerated.

For coding, instruction-following, and general knowledge tasks, Mozilla's report puts open models at or near parity with closed systems. This finding aligns with Stanford HAI's 2025 AI Index, which observed Chinese open models reaching near parity with U.S. frontier models on benchmarks like MMLU and HumanEval in 2024. The capability convergence is real on routine work.

But the 3.3% average hides something important. The gap is not uniform. On boilerplate code generation and text summarization, open models are genuinely competitive. On advanced reasoning, long-context retrieval, and agentic workflows, closed models maintain a real lead.

TIME raised this exact objection: if open models are at parity on coding but behind on reasoning. And complex coding requires reasoning, then the parity claim breaks down exactly where it matters most for business use cases.

My agency sees this split daily. We route high-volume content generation, summarization. And classification to open models where the quality bar is "good enough" and the cost bar is "as cheap as possible." For client-facing analysis, multi-step reasoning, and agentic workflows, we still use closed APIs. The 3.3% average masks domains where the gap is negligible and domains where it is decisive.

Knowing which side of that line your workload falls on is the difference between saving 80% on inference and shipping broken output.

The cost math has shifted hard in open's favor, though.

Mozilla reports that operational costs for open models have fallen roughly 50 times over three years. Workloads that were prohibitively expensive to self-host in 2023 are economically viable today. If you are still paying premium API rates for tasks that open models handle adequately, you are burning margin that could fund actual product development.

Why Do Open Models Only Capture 4% of Revenue?

This is the finding that should reframe how every small operator thinks about model economics. Open models handle approximately 33% of production AI tokens globally. They capture about 4% of global AI market revenue.

That gap is structural, not accidental.

Closed providers charge roughly 6 times more per call for comparable output quality on many tasks, according to Mozilla's analysis.

That premium is not pure margin. You are paying for the safety layer, the observability tooling, the API reliability, the support team. And the brand trust that comes with a named vendor. Open models give you the weights and leave everything else as an exercise for the reader.

Mozilla characterizes open source AI as a "real commercial layer" now, with paying customers and billions in revenue behind it. The success stories are concrete. Mistral, the Paris-based AI startup, reached $400 million in annual recurring revenue, up twentyfold in 12 months. Databricks is running at a $5.4 billion revenue rate following its acquisition of MosaicML in 2023 to expand into open model training. These are not hobby projects or academic experiments.

But here is the structural problem.

If open models carry a third of global AI traffic and collect a twenty-fifth of the revenue, the money is flowing to the wrapper, not the engine. Mozilla identifies operational tooling, deployment infrastructure, and trust gaps as the primary barriers. Closed providers sell you a bundle: model plus safety plus observability plus support. Open models sell you a weight file and point you to a Discord server.

For small agencies and solo operators, that is both the opportunity and the risk. The opportunity is straightforward: you can undercut closed providers on cost by 5-6x on comparable workloads and pass those savings to clients or keep them as margin. Risk: that you now own the orchestration stack, the monitoring, and the trust layer that closed providers handle automatically. If something goes wrong with an open model deployment at 2 AM, there is no enterprise support line to call.

What Is Actually Blocking Open Source AI From Production?

Mozilla attributes the deployment gap to operational hurdles rather than raw model performance.

The report points to shortcomings in orchestration layers, observability tooling, governance frameworks, and permission models around open systems. The plumbing, not the engine.

Mozilla also highlights a fragmentation problem within the open camp. Open-weight models (where weights are released but training details are withheld) are growing, while fully open-source models are declining. You cannot build a coordinated movement when participants disagree on what "open" actually means. This split weakens the collective case for open source AI and makes it harder to build shared infrastructure.

My read on this is straightforward. The model is becoming a commodity. The real fight has moved to the software layer that wraps it: the agentic runtime, the tool-calling framework, the memory system, the permission model. Closed providers invest heavily in that layer because it is where the lock-in lives. Open source alternatives exist, but they are fragmented and rarely production-grade without significant engineering investment.

That is the gap Mozilla wants to close.

Mozilla's strategy, as presented with the report, is to build a "rebel alliance" for open source AI to counter centralized tech monopolies. They want a LAMP-like open stack for AI: open interfaces, open data, open models. It is an ambitious vision that echoes the early web. Whether community-driven efforts can match the spending power of frontier labs is the genuinely open question the report raises but cannot answer.

What Should Small Operators Do Right Now?

Start with your API bill.

Pull the last month of calls and sort by task type. You will likely find that the majority of your traffic is routine work: summarization, drafting, classification, basic code completion. Those are the workloads where open models are within 3.3% of closed performance at a fraction of the cost.

Move one high-volume workload to an open model this month.

Measure the quality difference against your closed baseline. If the results are acceptable, move two more next month. The 50x cost reduction in open model operations over three years means the economics have crossed a threshold that most operators have not internalized yet.

Keep your closed-model integration for reasoning-heavy, multi-step work. That is where the gap is real and where the premium is justified. But stop paying 6x for tasks where the quality difference is invisible to your end user. Every dollar you save on routine inference is a dollar you can spend on the deployment infrastructure that actually differentiates your product.

Then invest in your deployment layer. This is where small operators can gain a real edge over enterprise teams that move slowly on infrastructure decisions. Solo operators and small agencies can build a proper open-model deployment pipeline in days, not quarters. The gap between open and closed model adoption is a tooling problem. And tooling problems are the kind small teams solve faster than large ones.

Mozilla's report confirms what many of us building with AI already suspected. The open-versus-closed fight is not about model quality anymore. It is about who controls the deployment stack and who captures the revenue. Open models are ready for your production traffic. The question is whether you are ready to build the infrastructure around them.

Start with one workload this week. Measure the savings. Then decide how much of your stack you want to own.

Sources

- Mozilla Blog: State of Open Source AI Report - Digital Journal: What Tech Leaders Should Take From Mozilla's Report - Developers Digest: Mozilla State of Open Source AI 2026 - TIME: Open Source AI Rebel Alliance - State of Open Source AI 2026 (PDF)

Comments ()